what is a safe harbor contribution to a 401k

What is a Safe Harbor 401(k) plan? What do you have to do to offer i? And what do all those acronyms mean?

Don't worry. We've helped many companies fix up compliant 401(k) plans, and we tin can walk you through all the basics. This guide explains everything from the unlike 401(k) compliance tests to what yous'll need to do to gear up a Safe Harbor program. It'south a trivial involved, though, and then let's start with some background information.

You lot probably already know that offering a 401(grand) makes it easier for employees at your company to save more for retirement. Simply the government wants to make sure that everyone — not just highly compensated employees — gets to participate in a meaningful way. The goal of 401(k) plans, afterwards all, is to ready more people for retirement, not to create a tax suspension that's exclusively for business owners and executives.

To brand certain anybody has a chance to do good from the plan their employer offers, the IRS has set a serial of what it calls "nondiscrimination" tests that are designed to measure out whether a 401(g) plan disproportionately favors highly compensated employees. If your plan were to fail 1 of these tests, information technology could mean making expensive corrections, a lot of administrative work, and potentially even refunding 401(thou) contributions.

And then, what'south a Safe Harbor 401(k) programme?

A Safe Harbor plan is a special kind of 401(1000) that automatically satisfies virtually nondiscrimination testing. It has certain built-in elements that are intended to help employees save by requiring companies to contribute to their employees' 401(chiliad) accounts. When employers take this step to encourage more employees to participate, the IRS offers them "rubber harbor" from both the nondiscrimination testing process and the consequences of failure.

If you're thinking about offering a Safe Harbor 401(k), hither's what you demand to know. Feel gratuitous to spring ahead if y'all're trying to answer a specific question:

- 401(chiliad) nondiscrimination tests

- Correcting a failing 401(k)

- Setting up a Safe Harbor 401(grand)

- Additional requirements for a Safe Harbor 401(grand)

- Pros and cons of a Safety Harbor 401(yard)

Ready? Okay, let'due south dive in.

What are nondiscrimination tests, and how do they affect your 401(chiliad) programme?

There are iii master types of nondiscrimination tests required past the IRS to help ensure that 401(thousand) plans benefit both owners and employees. Two of these tests compare how highly compensated employees (HCEs) and all other employees use your company's 401(1000):

The Bodily Deferral Pct (ADP) test measures how much income your HCEs contribute to their 401(1000), compared to rank and file employees.

The Actual Contribution Pct (ACP) exam is like, simply information technology compares employer contributions to HCEs with everyone else.

A third test, the Top-Heavy test, looks at individuals the IRS defines equally "key employees" and measures the value of the avails in their 401(grand) accounts, compared to all assets held in the 401(1000) plan. To become a detailed look at all these definitions, how the tests are applied, and see examples, check out our overview of the iii 401(m) nondiscrimination tests.

If your plan fails any of these tests, you lot'll have to deal with some administrative hassle, potentially expensive corrections, and the possibility of refunding 401(k) contributions. A Condom Harbor 401(k) tin can generally assist you avoid the uncertainty surrounding annual testing.*

Setting upwards a Safe Harbor 401(g) programme

Does passing these tests seem like a bit of a pain? If and then, and so a Prophylactic Harbor 401(yard) that's generally bachelor to all employees might be a better style to go depending on your specific circumstances.

Safe Harbor plans require that you lot contribute to your employees retirement 401(one thousand) accounts in i of ii forms: a lucifer or a nonelective contribution. This requirement is important because it can help increase savings. According to the Economic Policy Plant (EPI), close to half of all American families don't have whatever retirement savings, and amongst families nearing retirement, the median savings is just $17,000.

In exchange for letting your plan automatically satisfy about nondiscrimination testing, you'll have to follow some rules to make sure your plan benefits all your visitor'southward employees.

If these requirements are at all confusing, we'd be happy to help. Schedule a quick consult to get hands-on help setting upward your 401(one thousand).

Requirements for a Safe Harbor 401(k)

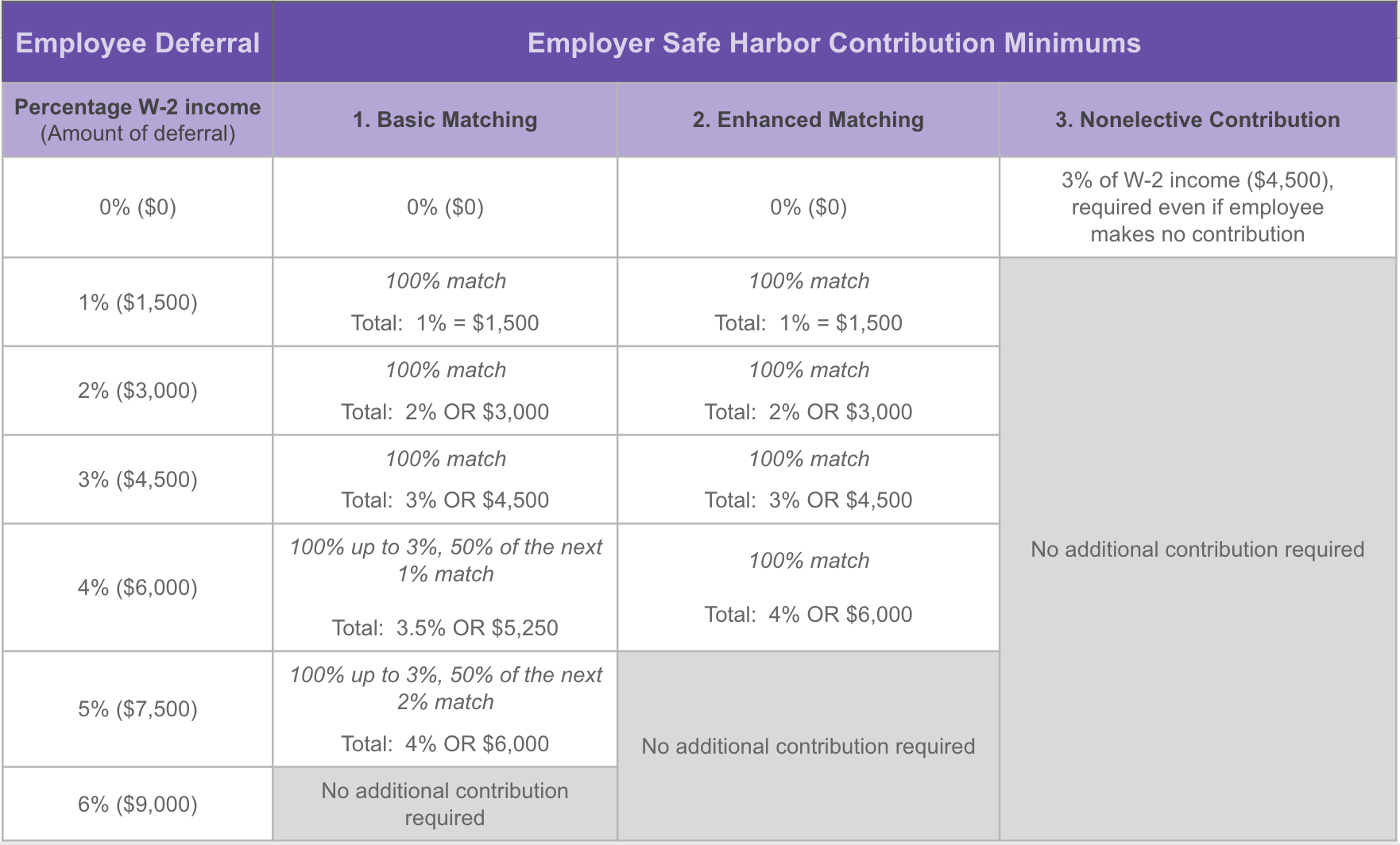

The primary requirement for a traditional Safe Harbor 401(k) is that the employer must brand contributions, and those contributions must vest immediately. Contributions can accept iii different forms, the first two of which are matching, which ways employees must defer funds to their accounts in order to receive contributions. The third option requires your visitor to make a contribution, fifty-fifty if employees don't defer any of their income into their plan.

Here are examples of the different contribution formulas:

1. Basic matching: The company matches 100% of all employee 401(k) contributions, up to 3% of their compensation, plus a fifty% match of the next 2% of their bounty

two. Enhanced matching: The visitor matches at to the lowest degree 100% of all employee 401(k) contributions, up to four% of their compensation (non to exceed 6% of compensation)

3. Not-elective contribution: The company contributes at to the lowest degree 3% of each employee'south compensation, regardless of whether employees brand contributions

This is what the matching and nonelective contributions would expect similar for an employee under the three unlike Condom Harbor formulas. The employee in this example earned $150,000 of eligible bounty during the twelvemonth.

Note that these contributions are only the minimums. For example, a more generous employer can lucifer upwardly to vi% of employees' pay, and it could still qualify as Safe Harbor.

Prophylactic Harbor contribution limits

In 2021, the basic employee deferral limits for a Rubber Harbor program are the same every bit any employer-sponsored 401(grand): $19,500 per year for participants under historic period 50, and $26,000 when y'all include grab-up contributions for employees over historic period 50 or older.

Equally an added benefit, with Safe Harbor provisions in place and less to to worry nigh when it comes to nondiscrimination testing, owners and highly compensated employees can truly max out their deferrals. That ways they can accept full advantage of their contribution limits.

Boosted Condom Harbor requirements

Making contributions to your employees' 401(k) is the about notable Prophylactic Harbor requirement, but in that location are additional rules surrounding when and how y'all offer your plan.

Prophylactic Harbor deadlines

For new plans, October 1 is the final borderline for starting a new Condom Harbor 401(k). But don't wait until a few days before the borderline to ready up your plan, because if you're making a matching contribution, you're also required to notify your employees 30 days earlier the plan starts, and it can take a week or more to set up your plan. And so, brand sure y'all talk to your 401(k) plan provider well before September 1. For existing plans, the deadlines depend on the blazon of Rubber Harbor contribution you are calculation to the plan and are detailed beneath.

Important dates for new plans:

- Baronial 20, 2021: Deadline for setting up your Guideline Safe Harbor 401(k) Program for the current yr.

- September 1, 2021: 30-24-hour interval notice must exist sent to employees

- Oct one, 2021: Safe Harbor 401(1000) Program is constructive and exempt from almost nondiscrimination testing for 2021.

It is of import to be enlightened that if a Safety Harbor feature is added to a new plan, information technology must exist in place for the entire plan year. If the plan year is fix retroactive to January one, contributions will be required based on eligible compensation for the unabridged yr.

Important dates for existing plans-Safe Harbor match

- November twenty, 2021: Deadline for requesting the addition of a Safe Harbor matching provision to your 401(k) plan with Guideline for the following year

- December i, 2021: xxx day discover must be sent to employees

- Jan 1, 2022: Safety Harbor provision takes effect for 2022

If you want to add a Condom Harbor matching provision to an existing 401(1000), your ambassador can make a programme subpoena that goes into consequence January i of any future year. Remember, there is an employee 30-day observe requirement, and it may have some time for your administrator to amend the programme, so endeavour to get this taken care of by the end of November to go into effect January 1. (At Guideline, November 21, 2021 is your last twenty-four hour period to add Safe Harbor matching provisions to your 401(g) to accept effect 2022.)

Important dates for existing plans-Rubber Harbor nonelective contributions

- November 30, 2021: Deadline for adopting the addition of a three% Safe Harbor Nonelective provision to your 401(k) plan with Guideline for the 2021 twelvemonth (request the amendment by November five, 2021)

- December 31, 2021: Borderline for adopting the addition of a iv% Safe Harbor Nonelective provision to your 401(k) plan with Guideline for the 2021 yr (request the amendment by December nine, 2022)

If you desire to add a Safety Harbor nonelective provision to an existing 401(one thousand) to take advantage of Safe Harbor condition for the year, y'all may practice so at any time earlier Dec 1st, so long as y'all are willing to pay the minimum 3% contribution for the entire plan year. After Dec 1st, you lot can still add a Safe Harbor nonelective contribution for the year in question, up to the borderline of Dec 31st of the following year, so long as yous increase the contribution to 4%. (Note: The new nonelective rule was passed by Congress in late 2019 under the SECURE Act and gives more than flexibility for those plans who didn't know they were going to neglect nondiscrimination testing and would like to rectify.)

Employee notice requirements

Each eligible employee must be notified in writing virtually their rights and obligations nether the program annually if the plan includes matching or automatic enrollment features. Discover must exist given inside a reasonable corporeality of time — at least xxx, but non more than 90 days — earlier the outset of the plan year.

Making mid-year changes to a Safe Harbor programme

If you already offering a Condom Harbor 401(thou) plan but would similar to make changes, there are special rules that you demand to follow and a few changes that are simply not immune. The details for mid-year changes are included in IRS Notice 2016-16. ( Note that the notice requirement for nonelective safe harbor plans that do not have a matching provision no longer apply).If the Condom Harbor plan has a match and you lot want to make changes, you must give employees an updated Safety Harbor notice that describes whatever changes. Find should be given xxx to ninety days before the changes go into effect and provide employees at least 30 days to modify their cash or deferral ballot. Safe Harbors plans can't change the type of Rubber Harbor (change from a match to a nonelective, for example) mid-yr and generally cannot reduce benefits under the program.

Once yous've satisfied the notice rules above, if applicative, you may be able to make changes to certain aspects of the programme including, for example, increasing hereafter Prophylactic Harbor nonelective contributions from 3% to four%, or changing the plan entry date for eligible employees from quarterly to monthly.

Several types of changes are not permissible during the year, all the same, and so review the rules carefully if yous wish to amend your plan.

If you already offering a Safe Harbor 401(chiliad) plan but would like to make changes, at that place are special rules that yous demand to follow. All the details for mid-year changes are included in IRS Notice 2016-16, merely these are the basic things the IRS requires:

- Give employees an updated Safety Harbor notice that describes any changes. Notice should exist given 30 to 90 days before the changes go into effect.

- Requite each notified employee at least 30 days to modify their cash or deferral election.

- A combined observe may be provided.

Once you've satisfied the notice rules above, you may be able to make changes to certain aspects of the plan including, for example, increasing futurity condom harbor non-elective contributions from iii% to 4%, or changing the plan entry date for eligible employees from quarterly to monthly.

Several types of changes are not permissible during the year, however, so review the rules carefully if you wish to meliorate your programme.

Is a Safe Harbor 401(k) plan right for my company?

Proficient question! In general, Safe Harbor plans are a adept selection for companies that practice any of the post-obit:

- Program to match employee contributions anyway

- Worry well-nigh passing nondiscrimination testing

- Fail the ADP, ACP, or Top-Heavy tests

- Have low participation amid NHCEs and non-fundamental employees

- Care deeply for the wellbeing of their employees

In terms of pros and cons, the biggest downside to offering a Safe Harbor plan is the cost of the contributions your company volition make. It'due south possible they could increase your overall payroll by iii% or more if all employees participate.

But many companies think the upside more than outweighs the toll. Offering a Safety Harbor 401(thou) plan can effect in happier employees, tax savings, and greater certainty that your plan won't fail nondiscrimination tests.

This content is for informational purposes but and is not intended to be construed equally tax communication. You should consult a tax professional to make up one's mind the best tax advantaged retirement plan for you.

*Rubber Harbor 401(k) plans mostly automatically satisfy Tiptop Heavy requirements, except for plan years in which the employer makes discretionary contributions (such as profit sharing contributions) in add-on to Prophylactic Harbor contributions.

Source: https://www.guideline.com/blog/safe-harbor-401k-plan/

0 Response to "what is a safe harbor contribution to a 401k"

Postar um comentário